What are principal components (PCs)?

Suppose we have a data matrix X with dimensions m x n, where each row corresponds to a different data point and each column corresponds to a different attribute. (For example, if we measured the height and weight of 1000 different people, then we could construct a data matrix with dimensions 1000 x 2.) Furthermore, let's presume that the mean of each column has been subtracted off (why this is important will become clear later). If we take the SVD of X, we obtain matrices U, S, and V such that X = U*S*V'. The columns of V are mutually orthogonal unit-length vectors; these are the principal components (PCs) of X.

SVD on the data matrix or the covariance matrix

Instead of taking the SVD of X (the data matrix), we can take the SVD of X'*X (the covariance matrix). This is because X'*X = (V*S'*U')*(U*S*V') = V*S.^2*V' (where S.^2 is a square matrix with the square of the diagonal entries of S along the diagonal). So, if we take the SVD of X'*X, the resulting V matrix should be identical to that obtained when taking the SVD of X (except for potential sign flips of the columns). A potential benefit of taking the SVD of the covariance matrix is reduced computational time. For example, if m >> n, then X is a large matrix of size m x n whereas X'*X is a small matrix of size n x n.

PCA decorrelates data

One way to think about PCA is that it decorrelates the data matrix. Prior to PCA, the columns of the data matrix may have some correlation with each other, i.e. the dot-product of any given pair of columns of X may be non-zero. What PCA does is to provide a linear transformation of the data such that after the transformation, the columns of the data matrix are uncorrelated with one another. The transformation is specifically given by multiplication with the matrix V.

What exactly does multiplication with V do? V has dimensions n x n and contains the principal components (PCs) in the columns. Given a point in n-dimensional space (i.e. a vector of dimensions 1 x n), if we multiply that point with V, what we are doing is projecting the point onto each of the PCs. This yields the coordinates of the point with respect to the space defined by the PCs. Since the PCs form an orthogonal basis, all we are really doing is rotating the space.

Now let's see what happens when we take the data matrix X and multiply it with V. Since X = U*S*V', X*V = U*S*V'*V = U*S. The result, U*S, has the property that the columns are uncorrelated with one another. The reason is that the columns of U are already mutually orthgonal by way of the SVD; and since S is a diagonal matrix, multiplication with S simply rescales the columns of U, which does not change the condition of mutual orthogonality.

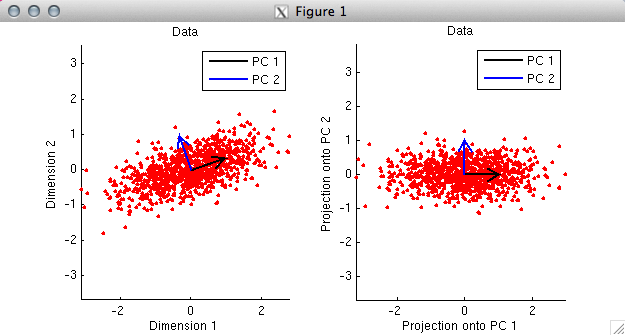

% Let's see an example. Here we create 1000 points

% in two-dimensional space.

X = zeromean(randnmulti(1000,[],[1 .6; .6 1],[1 .5]),1);

[U,S,V] = svd(X,0);

figure; setfigurepos([100 100 500 250]);

subplot(1,2,1); hold on;

scatter(X(:,1),X(:,2),'r.');

axis equal;

h1 = drawarrow([0 0],V(:,1)','k-',[],10,'LineWidth',2);

h2 = drawarrow([0 0],V(:,2)','b-',[],10,'LineWidth',2);

legend([h1 h2],{'PC 1' 'PC 2'});

xlabel('Dimension 1');

ylabel('Dimension 2');

title('Data');

subplot(1,2,2); hold on;

X2 = X*V;

V2 = (V'*V)';

scatter(X2(:,1),X2(:,2),'r.');

axis equal;

h1 = drawarrow([0 0],V2(:,1)','k-',[],10,'LineWidth',2);

h2 = drawarrow([0 0],V2(:,2)','b-',[],10,'LineWidth',2);

legend([h1 h2],{'PC 1' 'PC 2'});

xlabel('Projection onto PC 1');

ylabel('Projection onto PC 2');

title('Data');

% In the first panel, we plot the data as red dots. Notice

% that the two dimensions are moderately correlated with each other.

% By taking the SVD of the data, we obtain the PCs, and we plot

% the PCs as black and blue arrows. Notice that the PCs are

% orthogonal to each other. Also, notice that the first PC points

% in the direction along which the data tends to lie.

%

% In the second panel, we project the data onto the PCs and

% re-plot the data. Notice that the only thing that has

% happened is that the space has been rotated. In this new

% space, the data points are uncorrelated and the PCs are

% now aligned with the coordinate axes.

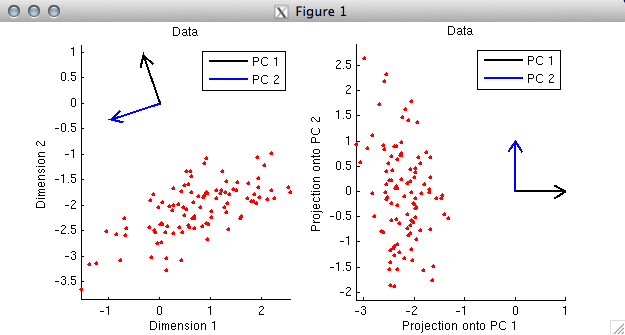

% Let's look at another example. Whereas in the previous example

% we ensured that the columns of the data matrix were zero-mean,

% in this example, we will intentionally make the columns have

% non-zero means.

X = randnmulti(100,[1 -2],[1 .7; .7 1],[1 .5]);

% (now repeat the code above)

% In this example, the first PC again points in the direction along

% which the data tend to lie. (Actually, strictly speaking, the

% first PC points in the opposite direction. But there is a sign

% ambiguity in SVD --- the signs of corresponding columns of the U

% and V matrices can be flipped with no change to the overall math.

% So if we wanted to, we could simply flip the sign of the first PC (which

% corresponds to the first column of V) and also flip the sign of

% the first column of U.) Notice that the first PC does not

% point in the direction of the elongation of the cloud of points;

% rather, the first PC points towards the middle of the cloud.

% The reason this happens is that the columns of the data matrix were not

% mean-subtracted (i.e. centered), and as it turns out, the primary effect

% in the data is displacement from the origin.

%

% (One consequence of neglecting to center each column is that the columns

% of the data matrix after projection onto the PCs may have some correlation

% with one another. After projection onto the PCs, it is guaranteed only

% that the dot-product of the columns is zero. Correlation (r) involves

% more than just a dot-product; it involves both mean-subtraction and

% unit-length-normalization before computing the dot product. Thus, there

% is no guarantee that the columns are uncorrelated. Indeed, in the

% previous example, the correlation after projection on the PCs is r=-0.23.)

%

% Whether or not to subtract off the mean of each data column before computing

% the SVD depends on the nature of the data --- it is up to you to decide.

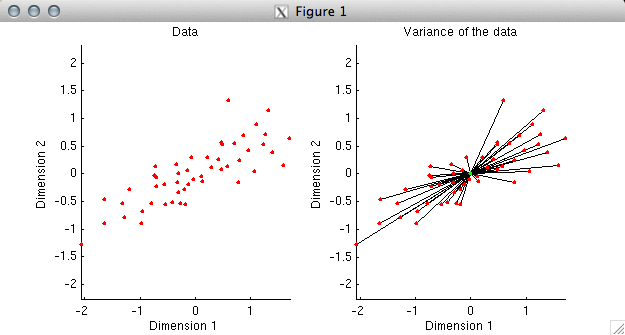

PCs point towards maximal variance in the data

% Principal components have a particular ordering --- each principal

% component points in the direction of maximal variance that is

% orthogonal to each of the previous principal components. In this

% way, each principal component accounts for the maximal possible

% amount of variance, ignoring the variance already accounted for

% by the previous principal components. (With respect to explaining

% variance, it would be pointless for a given vector to be

% non-orthogonal to all previous ones; the extra descriptive

% power afforded by a vector lies only in the component of the

% vector that is orthogonal to the existing subspace.)

% Let's see an example.

X = zeromean(randnmulti(50,[],[1 .8; .8 1],[1 .5]),1);

figure; setfigurepos([100 100 500 250]);

subplot(1,2,1); hold on;

scatter(X(:,1),X(:,2),'r.');

axis equal;

xlabel('Dimension 1');

ylabel('Dimension 2');

title('Data');

subplot(1,2,2); hold on;

h = [];

for p=1:size(X,1)

h(p) = plot([0 X(p,1)],[0 X(p,2)],'k-');

end

scatter(X(:,1),X(:,2),'r.');

scatter(0,0,'g.');

axis equal; ax = axis;

xlabel('Dimension 1');

ylabel('Dimension 2');

title('Variance of the data');

% In the first plot, we simply plot the data. Before

% proceeding, we need to understand what it means to explain

% variance in data. Variance (without worrying about

% mean-subtraction or the normalization term) is simply the

% sum of the squares of the values in a given set of data.

% Now, since the sum of the squares of the coordinates of a

% data point is the same as the square of the distance of the

% data point from the origin, we can think of variance as

% equivalent to squared distance. To illustrate this, in the

% second plot we have drawn a black line between each data

% point and the origin. The aggregate of all of the black lines

% can be thought of as representing the variance of the data.

% If we have a model that is attempting to fit the data, we

% can ask how close the model comes to the data points.

% The closer that the model is to the data, the more variance

% the model explains in the data. Currently, without a model,

% our model fit is simply the origin, and we have 100% of the

% variance left to explain.

%

% What we would like to determine is the direction that accounts

% for maximal variance in the data. That is, we are looking for

% a vector such that if we were to use that vector to fit the

% data points, the fitted points would be as close to the data

% as possible.

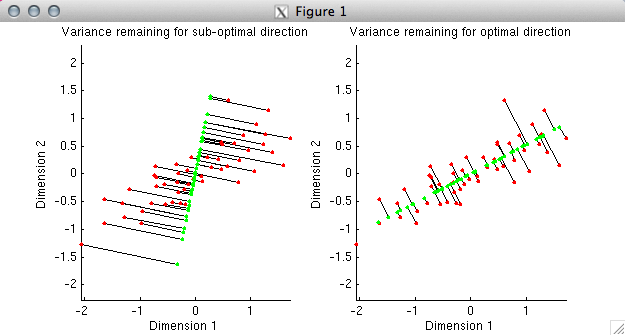

figure; setfigurepos([100 100 500 250]);

subplot(1,2,1); hold on;

direction = unitlength([.2 1]');

Xproj = X*direction*direction';

h = [];

for p=1:size(X,1)

h(p) = plot([Xproj(p,1) X(p,1)],[Xproj(p,2) X(p,2)],'k-');

end

h0 = scatter(X(:,1),X(:,2),'r.');

h1 = scatter(Xproj(:,1),Xproj(:,2),'g.');

axis(ax);

xlabel('Dimension 1');

ylabel('Dimension 2');

title('Variance remaining for sub-optimal direction');

subplot(1,2,2); hold on;

[U,S,V] = svd(X,0);

direction = V(:,1);

Xproj = X*direction*direction';

h = [];

for p=1:size(X,1)

h(p) = plot([Xproj(p,1) X(p,1)],[Xproj(p,2) X(p,2)],'k-');

end

h0 = scatter(X(:,1),X(:,2),'r.');

h1 = scatter(Xproj(:,1),Xproj(:,2),'g.');

axis(ax);

xlabel('Dimension 1');

ylabel('Dimension 2');

title('Variance remaining for optimal direction');

% In the first plot, we have deliberately chosen a sub-optimal

% direction (the direction points slightly to the right of vertical).

% Using the given direction, we have determined the best possible fit

% to each data point; the fitted points are shown in green. The

% distance from the fitted points to the actual data points is

% indicated by black lines. In the second plot, we have chosen the

% optimal direction, namely, the first principal component of the data.

% Notice that the total distance from the fitted points to the actual data

% points is much smaller in the second case than in the first. This

% reflects the fact that the first principal component explains much

% more variance than the direction we chose in the first plot.

%

% The idea, then, is to repeat this process iteratively --- first,

% we determine the vector that approximates the data as best as

% possible, then we add in a second vector that improves the

% approximation as much as possible, and so on.

Singular values indicate variance explained

% A nice characteristic of PCA is that the PCs define

% an orthogonal coordinate system. Because of this property,

% the incremental improvements with which the PCs approximate

% the data are exactly additive.

%

% (To see why, imagine you have a point that is located at (x,y,z).

% The squared distance to the origin is x^2+y^2+z^2.

% If we use the x-axis to approximate the point,

% the model fit is (x,0,0) and the remaining distance is

% y^2+z^2. If we then use the y-axis to approximate the point,

% the model fit is (x,y,0) and the remaining distance is

% z^2. Finally, if we use the z-axis to approximate the point,

% the model fit is (x,y,z) and there is zero remaining distance.

% Thus, due to the geometric properties of Euclidean space, all

% of the variance components add up exactly.)

%

% A little math can show that that the variance accounted

% for by individual principal components is given by the square of

% diagonal elements of the matrix S (which are also known as

% the singular values).

%

% The proportion of the total variance in a dataset that

% is accounted for by the first N PCs, where N ranges

% from 1 to the number of dimensions in the data can

% be calculated simply as

% cumsum(diag(S).^2) / sum(diag(S).^2) * 100.

% This sequence of percentages is useful when choosing

% a small number of PCs to summarize a dataset.

% We will see an example of this below.

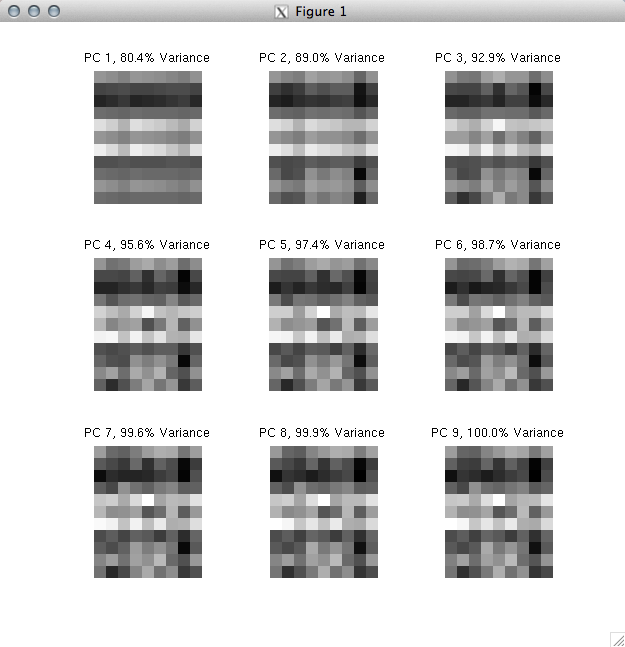

Matrix reconstruction

% In data exploration, it is often useful to look at the big

% effects in the data. A quick and dirty technique is to identify

% a small number of PCs that define a subspace within which

% most of the data resides.

temp = unitlength(rand(100,9),1);

X = randnmulti(11,rand(1,9),temp'*temp);

[U,S,V] = svd(X,0);

varex = cumsum(diag(S).^2) / sum(diag(S).^2) * 100;

Xapproximate = [];

for p=1:size(X,2)

% this is a nice trick for using the first p principal

% components to approximate the data matrix. we leave it

% to the reader to verify why this works.

Xapproximate(:,:,p) = U(:,1:p)*S(1:p,1:p)*V(:,1:p)';

end

mn = min(X(:));

mx = max(X(:));

figure; setfigurepos([100 100 500 500]);

for p=1:size(X,2)

subplot(3,3,p); hold on;

imagesc(Xapproximate(:,:,p),[mn mx]);

axis image; axis off;

title(sprintf('PC %d, %.1f%% Variance',p,varex(p)));

end

% What we have done here is to create a dataset (dimensions 11 x 9)

% and then use an increasing number of PCs to approximate the data.

% The full dataset corresponds to "PC 9" where we use all 9

% PCs to approximate the data. Notice that using just 3 PCs

% allows us to account for 92.9% of the variance in the original data.

%

% A useful next step might be to try and interpret the first 3 PCs

% and/or to visualize the data projected onto the first 3 PCs.

% If we gained an understanding of what is happening in the

% first 3 PCs of the data, it would probably be safe to deem that we

% have a good understanding of the data.

I really like how you explain the PCA analysis in a simple/lucid manner with illustrative matlab examples! Keep up the good work and it would be great to see more posts about different statistical techniques!

ReplyDeleteReally very nice blog information for this one and more technical skills are improve,i like that kind of post.

ReplyDeleteClick here:

angularjs training in btm

Click here:

angularjs training in rajajinagar

Click here:

angularjs training in marathahalli

Click here:

angularjs training in bangalore

Click here:

angularjs training in pune

I would assume that we use more than the eyes to gauge a person's feelings. Mouth. Body language. Even voice. You could at least have given us a face in this test.

ReplyDeleteClick here:

Microsoft azure training in velarchery

Click here:

Microsoft azure training in sollinganallur

Click here:

Microsoft azure training in btm

Click here:

Microsoft azure training in rajajinagar

Wonderful bloggers like yourself who would positively reply encouraged me to be more open and engaging in commenting.So know it's helpful.

ReplyDeleteBlueprism training in Chennai

Blueprism training in Bangalore

Blueprism training in Pune

Blueprism online training

Blueprism training in tambaram

Wonderful bloggers like yourself who would positively reply encouraged me to be more open and engaging in commenting.So know it's helpful.

ReplyDeleteBlueprism training in Chennai

Blueprism training in Bangalore

Blueprism training in Pune

Blueprism online training

Blueprism training in tambaram

After seeing your article I want to say that the presentation is very good and also a well-written article with some very good information which is very useful for the readers....thanks for sharing it and do share more posts like this.

ReplyDeleteData Science course in kalyan nagar | Data Science course in OMR

Data Science course in chennai | Data science course in velachery

Data science course in jaya nagar | Data science training in tambaram

Inspiring writings and I greatly admired what you have to say , I hope you continue to provide new ideas for us all and greetings success always for you..Keep update more information..

ReplyDeletejava training in tambaram | java training in velachery

java training in omr | oracle training in chennai

I really enjoy simply reading all of your weblogs. Simply wanted to inform you that you have people like me who appreciate your work. Definitely a great post I would like to read this

ReplyDeleteangularjs Training in bangalore

angularjs Training in bangalore

angularjs Training in btm

angularjs Training in electronic-city

angularjs online Training

angularjs Training in marathahalli

This is quite educational arrange. It has famous breeding about what I rarity to vouch. Colossal proverb. This trumpet is a famous tone to nab to troths. Congratulations on a career well achieved. This arrange is synchronous s informative impolites festivity to pity. I appreciated what you ok extremely here

ReplyDeleteinformatica mdm online training

apache spark online training

angularjs online training

devops online training

aws online training

Awesome! Education is the extreme motivation that open the new doors of data and material. So we always need to study around the things and the new part of educations with that we are not mindful.

ReplyDeleteMicrosoft Azure online training

Selenium online training

Java online training

Python online training

uipath online training

Your info is really amazing with impressive content..Excellent blog with informative concept. Really I feel happy to see this useful blog, Thanks for sharing such a nice blog..

ReplyDeleteIf you are looking for any Data science Related information please visit our website Data science courses in Pune page!

really very nice blog.

ReplyDeleteBEST ANGULAR JS TRAINING IN CHENNAI WITH PLACEMENT

https://www.acte.in/angular-js-training-in-chennai

https://www.acte.in/angular-js-training-in-annanagar

https://www.acte.in/angular-js-training-in-omr

https://www.acte.in/angular-js-training-in-porur

https://www.acte.in/angular-js-training-in-tambaram

https://www.acte.in/angular-js-training-in-velachery

Its an amazing and wonderful site to visit.

ReplyDeleteAngularJS training in chennai | AngularJS training in anna nagar | AngularJS training in omr | AngularJS training in porur | AngularJS training in tambaram | AngularJS training in velachery

This Was An Amazing ! I Haven't Seen This Type of Blog Ever ! Thankyou For Sharing,thanks a lot.

ReplyDeleteAi & Artificial Intelligence Course in Chennai

PHP Training in Chennai

Ethical Hacking Course in Chennai Blue Prism Training in Chennai

UiPath Training in Chennai

The blog gives more information about the training and career, its useful to enhance my skills and knowledge.

ReplyDeleteOracle Training | Online Course | Certification in chennai | Oracle Training | Online Course | Certification in bangalore | Oracle Training | Online Course | Certification in hyderabad | Oracle Training | Online Course | Certification in pune | Oracle Training | Online Course | Certification in coimbatore

I greatly admired what you have to say , I hope you continue to provide new ideas.

ReplyDeletePython Training in Chennai

Python Training in Bangalore

Python Training in Hyderabad

Python Training in Coimbatore

Python Training

python online training

python flask training

python flask online training

Thanks for sharing such a great information.

ReplyDeleteWeb design Training in Chennai

Web design Training in Velachery

Web design Training in Tambaram

Web design Training in Porur

Web design Training in Omr

Web design Training in Annanagar

I truly appreciate this post about Web Design. I’ve been looking all over for this! Thank goodness I found it on your blog

ReplyDeleteamazon web services aws training in chennai

microsoft azure training in chennai

workday training in chennai

android-training-in chennai

ios training in chennai

Nice Blog !

ReplyDeleteOne such issue is QuickBooks Error 80070057. Due to this error, you'll not be able to work on your software. Thus, to fix these issues, call us at 1-855-977-7463 and get the best ways to troubleshoot QuickBooks queries.

v

ReplyDeleteInfycle Technologies in Chennai offers the leading Big Data Hadoop Training in Chennai for tech professionals and students at the best offers. In addition to the Python course, other in-demand courses such as Data Science, Big Data Selenium, Oracle, Hadoop, Java, Power BI, Tableau, Digital Marketing also will be trained with 100% practical classes. Dial 7504633633 to get more info and a free demo.

This post is so usefull and informaive keep updating with more information.....

ReplyDeleteBest Selenium Training in Bangalore

Selenium Training Institute in Bangalore

Great Post!!! Thanks for sharing this great post.

ReplyDeleteWhat are the Applications of Java?

Applications of Java

Uşak

ReplyDeleteAnkara

Adıyaman

Hatay

Şırnak

PQMM

Erzurum

ReplyDeleteistanbul

Ağrı

Malatya

Trabzon

8V2Q

https://titandijital.com.tr/

ReplyDeletesivas parça eşya taşıma

mardin parça eşya taşıma

karaman parça eşya taşıma

manisa parça eşya taşıma

XFVANA

ankara parça eşya taşıma

ReplyDeletetakipçi satın al

antalya rent a car

antalya rent a car

ankara parça eşya taşıma

WMNRXR

maraş evden eve nakliyat

ReplyDeleteosmaniye evden eve nakliyat

adıyaman evden eve nakliyat

istanbul evden eve nakliyat

ordu evden eve nakliyat

FEGB

ığdır evden eve nakliyat

ReplyDeleteağrı evden eve nakliyat

maraş evden eve nakliyat

diyarbakır evden eve nakliyat

şırnak evden eve nakliyat

V4R

https://istanbulolala.biz/

ReplyDelete62VEWR

karabük evden eve nakliyat

ReplyDeletebartın evden eve nakliyat

maraş evden eve nakliyat

mersin evden eve nakliyat

aksaray evden eve nakliyat

WVA1

düzce evden eve nakliyat

ReplyDeletedenizli evden eve nakliyat

kırşehir evden eve nakliyat

çorum evden eve nakliyat

afyon evden eve nakliyat

0P1SİC

8F0AD

ReplyDeleteNiğde Parça Eşya Taşıma

Karaman Evden Eve Nakliyat

Çankırı Evden Eve Nakliyat

Batman Evden Eve Nakliyat

Zonguldak Parça Eşya Taşıma

C9251

ReplyDeleteAfyon Lojistik

Diyarbakır Şehirler Arası Nakliyat

Ağrı Parça Eşya Taşıma

Chat Gpt Coin Hangi Borsada

Kilis Lojistik

Sinop Şehir İçi Nakliyat

Ordu Evden Eve Nakliyat

Elazığ Lojistik

Pursaklar Parke Ustası

FDB12

ReplyDeleteAfyon Lojistik

Kripto Para Borsaları

Fuckelon Coin Hangi Borsada

Kütahya Lojistik

Bingöl Evden Eve Nakliyat

İzmir Şehirler Arası Nakliyat

Mersin Parça Eşya Taşıma

Antalya Şehir İçi Nakliyat

Referans Kimliği Nedir

36099

ReplyDeleteKırıkkale Evden Eve Nakliyat

Maraş Evden Eve Nakliyat

Çerkezköy Boya Ustası

Sakarya Şehirler Arası Nakliyat

Kastamonu Şehir İçi Nakliyat

Yobit Güvenilir mi

Uşak Şehirler Arası Nakliyat

Arbitrum Coin Hangi Borsada

Bilecik Evden Eve Nakliyat

68F78

ReplyDeletetokat sesli sohbet siteler

ığdır mobil sohbet odaları

nevşehir kızlarla canlı sohbet

afyon sesli görüntülü sohbet

kadınlarla rastgele sohbet

urfa kadınlarla rastgele sohbet

artvin mobil sohbet sitesi

aydın rastgele sohbet uygulaması

niğde canlı ücretsiz sohbet

BA39E

ReplyDeleteardahan en iyi ücretsiz sohbet siteleri

canlı sohbet odaları

tekirdağ canlı sohbet sitesi

van en iyi görüntülü sohbet uygulamaları

yabancı görüntülü sohbet uygulamaları

aydın sohbet sitesi

samsun ücretsiz sohbet

trabzon rastgele sohbet siteleri

malatya telefonda sohbet

81887

ReplyDeleteBinance Referans Kodu

Tiktok Beğeni Satın Al

Bulut Madenciliği Nedir

Mexc Borsası Kimin

Nonolive Takipçi Satın Al

Bitcoin Kazanma Siteleri

Parasız Görüntülü Sohbet

Shibanomi Coin Hangi Borsada

Star Atlas Coin Hangi Borsada

87665

ReplyDeleteDazkırı

Yığılca

Köyceğiz

Gürgentepe

Kadirli

Gümüşova

Şavşat

Şahinbey

Gerger

We are seeking dedicated and compassionate nurses to join our healthcare team in the UK. The ideal candidates will hold a valid nursing license and possess excellent clinical skills. As part of our team, you will provide high-quality patient care, work collaboratively with other healthcare professionals, and ensure adherence to established protocols. We offer competitive salaries, professional development opportunities, and supportive working environments. Candidates must demonstrate strong communication abilities and a commitment to patient-centered care. Apply now to be a part of a dynamic healthcare setting, enhancing patient outcomes and advancing your nursing career in the UK.

ReplyDeletehttps://www.dynamichealthstaff.com/nurses-job-vacancy-in-uk

Principal components analysis (PCA) is a powerful statistical technique used to reduce data dimensionality while preserving variance. For businesses like yellowstone clothing, PCA can help identify key factors influencing customer preferences, streamlining inventory and marketing strategies to enhance customer experience and optimize product offerings effectively.

ReplyDeleteشركة عزل خزانات بخميس مشيط h9hbw7a90V

ReplyDeleteشركة عزل خزانات بخميس مشيط 5vtg5XabCw

ReplyDeleteشركة عزل خزانات بخميس مشيط CKSKiEZqA7

ReplyDeleteشركة مكافحة حشرات بالاحساء sFirkpGmM4

ReplyDeleteشركة مكافحة حشرات بخميس مشيط

ReplyDeletejsl1wNUhsc

B1BC31FE81

ReplyDeletetürk takipçi

beğeni satın al

takipçi paketi

gerçek takipçi

fake takipçi

5A4AD81D08

ReplyDeleteinstagram takipçi al

youtube beğeni satın al

ucuz takipçi

bayan takipçi

telafili takipçi

Principal Component Analysis (PCA) is a crucial statistical method widely used for reducing the dimensionality of large datasets while retaining the maximum variance. It helps in simplifying complex data, making patterns clearer, and supporting better decision-making. Students often confuse PCA with business tools like SWOT, but both play crucial roles in analysis. While PCA deals with data transformation and visualization, SWOT focuses on identifying strengths, weaknesses, opportunities, and threats. If you are working on academic tasks, especially case studies, combining both approaches can be powerful. For detailed guidance, students can explore SWOT analysis assignment help to strengthen their learning.

ReplyDelete